If you're applying for a loan, a credit card, or even a mortgage, understanding the role of hard inquiries is crucial. A hard inquiry occurs when a lender checks your credit report to assess your creditworthiness. While it’s a standard part of the lending process, it can temporarily affect your credit score. Knowing how long a hard inquiry affects credit can help you make informed financial decisions and minimize any negative impact. Credit scores play a pivotal role in determining your financial future. They influence everything from loan approvals to interest rates, making it essential to monitor what affects them. Hard inquiries are one of the factors that can lower your score, albeit temporarily. Typically, a hard inquiry remains on your credit report for two years, but its impact on your credit score diminishes after a few months. This article will delve into the nuances of hard inquiries, explaining how they work, their duration, and how you can manage them effectively. So, whether you're planning to apply for multiple credit cards or a large loan, this guide will equip you with the knowledge to navigate hard inquiries confidently. We’ll explore strategies to minimize their impact, understand their role in credit scoring, and answer common questions about how long a hard inquiry affects credit. By the end of this article, you’ll have a comprehensive understanding of this critical aspect of credit management.

Table of Contents

- What Is a Hard Inquiry and Why Does It Matter?

- How Long Does a Hard Inquiry Affect Credit?

- Why Do Hard Inquiries Impact Credit Scores?

- Can Multiple Hard Inquiries Hurt Your Credit Score?

- How to Minimize the Impact of Hard Inquiries?

- What Are the Differences Between Hard and Soft Inquiries?

- Are There Any Loopholes to Avoid Hard Inquiries?

- How Can You Monitor Your Credit Report for Hard Inquiries?

What Is a Hard Inquiry and Why Does It Matter?

A hard inquiry, also known as a "hard pull," occurs when a financial institution, such as a bank or credit card issuer, reviews your credit report as part of a lending decision. This type of inquiry is initiated when you apply for credit products like loans, credit cards, or mortgages. Unlike soft inquiries, which are typically initiated for background checks or pre-approval offers, hard inquiries can affect your credit score. They signal to lenders that you are actively seeking new credit, which could indicate financial instability if done excessively. The importance of understanding hard inquiries lies in their potential impact on your credit score. While a single hard inquiry might only lower your score by a few points, multiple inquiries within a short period can raise red flags for lenders. This is because frequent credit applications may suggest that you are overextending yourself financially. However, not all hard inquiries are treated equally. For example, if you're shopping around for the best mortgage or auto loan rate, credit scoring models often group multiple inquiries within a short timeframe as a single inquiry. To better understand how hard inquiries work, consider the following points:

- Hard inquiries are recorded on your credit report and visible to lenders.

- They typically remain on your report for two years but only affect your score for about 12 months.

- Not all credit checks result in hard inquiries; only those initiated by your application for credit do.

How Long Does a Hard Inquiry Affect Credit?

The burning question on many people's minds is, "How long does a hard inquiry affect credit?" The answer depends on several factors, but generally, a hard inquiry can stay on your credit report for up to two years. However, its impact on your credit score is usually limited to the first 6 to 12 months. After this period, the effect diminishes significantly, and it no longer plays a role in determining your creditworthiness. Credit scoring models, such as FICO and VantageScore, weigh hard inquiries as a minor factor compared to other elements like payment history or credit utilization. Typically, a single hard inquiry might lower your credit score by less than five points. However, the cumulative effect of multiple inquiries can be more substantial, especially if they occur within a short timeframe. For instance, applying for several credit cards in quick succession could signal to lenders that you're taking on too much debt, which could hurt your credit score. To better understand the timeline of hard inquiries, here’s a breakdown:

Read also:Exploring The Essence Of Warmth Chapter 3 Jackerman A Comprehensive Guide

- Immediate Impact: A hard inquiry can lower your score by a few points immediately after it occurs.

- Short-Term Effect (6–12 months): During this period, the inquiry remains a factor in your credit score but gradually diminishes in importance.

- Long-Term Visibility (Up to 2 years): While the inquiry stays on your report for two years, it no longer affects your score after 12 months.

How Can You Track the Duration of a Hard Inquiry?

If you're curious about how long a hard inquiry remains on your credit report, the best way to track it is by regularly reviewing your credit report. You can obtain a free copy of your credit report from each of the three major credit bureaus—Equifax, Experian, and TransUnion—once a year through AnnualCreditReport.com. By monitoring your report, you can ensure that no unauthorized inquiries are made and that legitimate ones are accurately recorded.

Does the Type of Loan Affect How Long a Hard Inquiry Impacts Credit?

The type of loan you're applying for can influence how hard inquiries are treated. For example, when shopping for a mortgage or auto loan, credit scoring models often group multiple inquiries within a 14–45 day window as a single inquiry. This "rate shopping" adjustment helps minimize the impact on your credit score, as it assumes you're comparing offers rather than seeking multiple loans.

Why Do Hard Inquiries Impact Credit Scores?

Hard inquiries are considered a risk factor by credit scoring models because they indicate that you're actively seeking new credit. Lenders view multiple credit applications as a potential sign of financial distress, which could increase the likelihood of default. While a single hard inquiry might not raise significant concerns, a pattern of frequent inquiries could signal to lenders that you're overextending yourself financially. The impact of hard inquiries on your credit score is relatively small compared to other factors like payment history or credit utilization. However, they can still play a role in determining your creditworthiness, especially if you have a limited credit history. For example, if you're a young borrower with only a few accounts, a hard inquiry could have a more pronounced effect on your score. To mitigate the impact of hard inquiries, consider the following tips:

- Limit the number of credit applications you submit within a short period.

- Take advantage of rate shopping windows for mortgages and auto loans.

- Regularly review your credit report to ensure accuracy.

Can Multiple Hard Inquiries Hurt Your Credit Score?

The short answer is yes—multiple hard inquiries can hurt your credit score, but the extent of the damage depends on several factors. If you apply for multiple credit cards or loans within a short timeframe, it could signal to lenders that you're financially overextended. This perception can lead to a more significant drop in your credit score, as lenders may view you as a higher-risk borrower. However, not all multiple inquiries are treated the same. For instance, credit scoring models like FICO and VantageScore recognize that consumers often shop around for the best rates on mortgages, auto loans, and student loans. As a result, they group multiple inquiries for these types of loans within a specific timeframe (usually 14–45 days) as a single inquiry. This adjustment helps protect your credit score from unnecessary drops due to rate shopping. To avoid the negative impact of multiple hard inquiries, consider the following strategies:

- Space out your credit applications to avoid clustering inquiries.

- Focus on rate shopping within a short timeframe to benefit from the grouping adjustment.

- Avoid applying for new credit unless absolutely necessary.

What Happens If You Have Too Many Hard Inquiries?

If you accumulate too many hard inquiries, it could raise concerns for lenders and lower your credit score. While the exact impact varies depending on your overall credit profile, excessive inquiries could signal financial instability. To address this, it’s essential to monitor your credit report regularly and dispute any unauthorized inquiries.

How to Minimize the Impact of Hard Inquiries?

While hard inquiries are sometimes unavoidable, there are steps you can take to minimize their impact on your credit score. One effective strategy is to limit the number of credit applications you submit within a short period. This approach helps prevent multiple inquiries from clustering and reduces the risk of lowering your score. Another way to minimize the impact is to take advantage of rate shopping windows for mortgages, auto loans, and student loans. Credit scoring models recognize that consumers often compare offers to secure the best rates, so they group multiple inquiries for these loans within a specific timeframe as a single inquiry. By timing your applications strategically, you can reduce the negative impact on your credit score. Here are some additional tips to minimize the impact of hard inquiries:

Read also:Danny Bonaduce The Life And Legacy Of A Child Star Turned Radio Icon

- Regularly review your credit report to ensure accuracy and dispute unauthorized inquiries.

- Consider using pre-qualification tools that rely on soft inquiries instead of hard pulls.

- Avoid applying for new credit unless absolutely necessary, especially if you're planning a major financial decision like buying a home.

Are There Tools to Help You Avoid Hard Inquiries?

Yes, several tools and services can help you avoid unnecessary hard inquiries. For example, many credit card issuers and lenders offer pre-qualification tools that use soft inquiries to assess your eligibility. These tools allow you to check your chances of approval without impacting your credit score.

What Are the Differences Between Hard and Soft Inquiries?

Understanding the differences between hard and soft inquiries is crucial for managing your credit effectively. A hard inquiry occurs when you apply for credit, and it requires your permission. It can affect your credit score and is visible to lenders. On the other hand, a soft inquiry is typically initiated for background checks, pre-approval offers, or when you check your own credit report. Soft inquiries do not impact your credit score and are only visible to you. To summarize the key differences:

- Hard Inquiries: Require your consent, affect your credit score, and are visible to lenders.

- Soft Inquiries: Do not require your consent, do not affect your credit score, and are only visible to you.

Are There Any Loopholes to Avoid Hard Inquiries?

While there’s no foolproof way to avoid hard inquiries entirely, there are strategies to reduce their frequency. One approach is to use pre-qualification tools that rely on soft inquiries to assess your eligibility. These tools allow you to check your chances of approval without triggering a hard pull on your credit report. Another strategy is to consolidate your credit applications within a short timeframe when shopping for loans. Credit scoring models often group multiple inquiries for mortgages, auto loans, and student loans as a single inquiry if they occur within a specific period. This adjustment helps minimize the impact on your credit score.

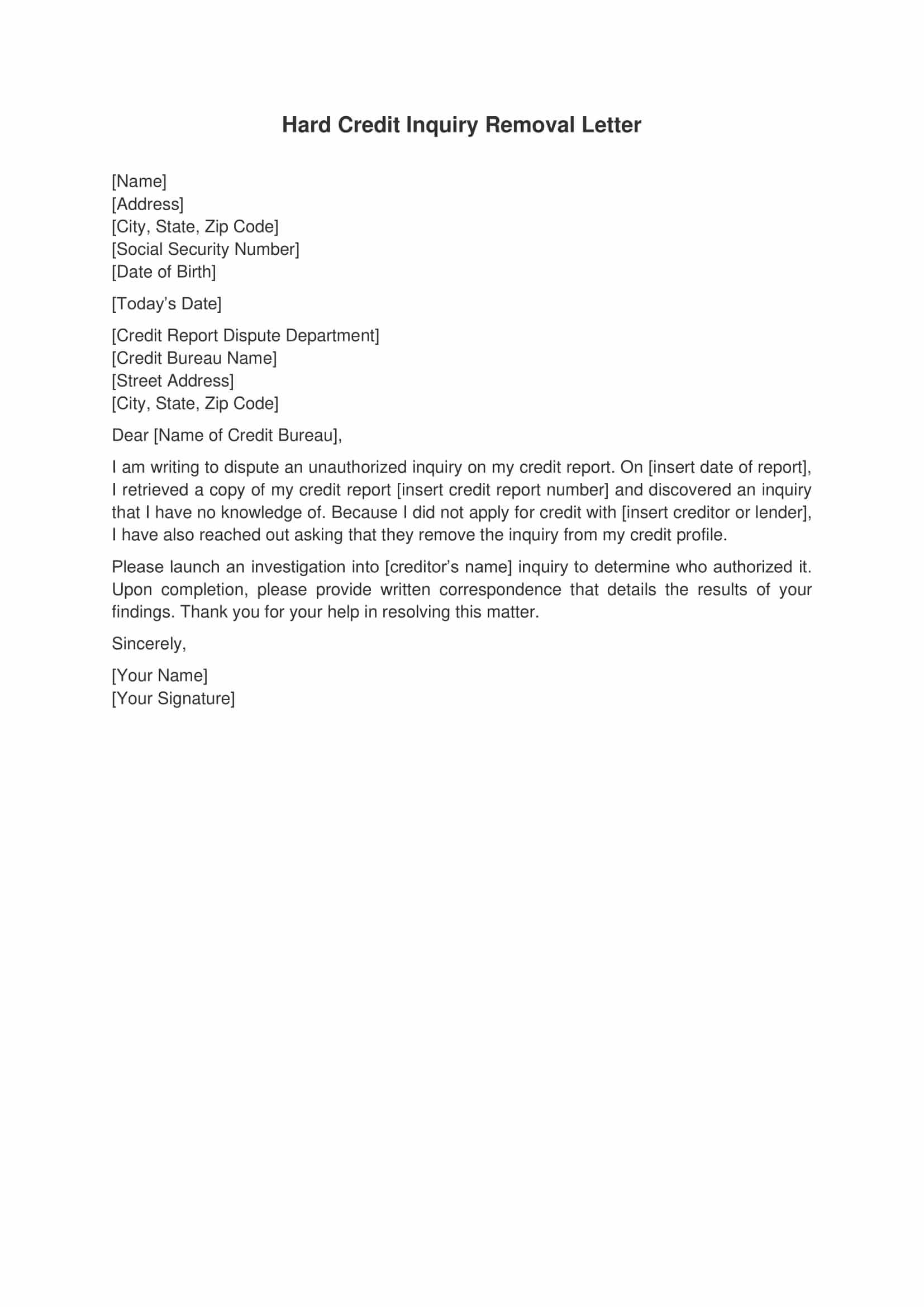

Can You Dispute Hard Inquiries?

If you notice unauthorized hard inquiries on your credit report, you have the right to dispute them. Start by contacting the credit bureau that issued the report and provide evidence to support your claim. If the inquiry is deemed unauthorized, it will be removed from your report, and its impact on your credit score will be eliminated.

How Can You Monitor Your Credit Report?

Monitoring your credit report is essential for managing hard inquiries and maintaining a healthy credit score. You can obtain a free copy of your credit report from each of the three major credit bureaus—Equifax, Experian, and TransUnion—once a year through AnnualCreditReport.com. By reviewing your report regularly, you can identify unauthorized inquiries and address any inaccuracies promptly. Consider using credit monitoring services to stay informed about changes to your credit report. These services alert you to new inquiries, account openings, and other activities that could impact your credit score. By staying proactive, you can protect your financial health and minimize the impact of hard inquiries.

Frequently Asked Questions

How Long Does a Hard Inquiry Affect Credit?