Have you ever wondered how long a hard inquiry stays on your credit report and what it means for your financial health? A hard inquiry occurs when a lender checks your credit report as part of a decision-making process, typically for loan or credit card approval. This action can have a temporary impact on your credit score, making it crucial to understand its duration and implications. Whether you're planning to apply for a mortgage, car loan, or credit card, knowing how long a hard inquiry remains visible to other lenders is essential for maintaining a strong credit profile.

Hard inquiries are a normal part of the credit application process, but they can sometimes raise concerns for borrowers. While a single hard inquiry may only cause a minor dip in your credit score, multiple inquiries in a short period can signal financial instability to lenders. This article dives deep into the mechanics of hard inquiries, their lifespan on your credit report, and strategies to minimize their impact. By the end, you'll have a clear understanding of how to manage hard inquiries effectively and maintain a healthy credit score.

Understanding the nuances of hard inquiries can help you make informed financial decisions. This article explores not only how long a hard inquiry stays on your credit report but also answers common questions like "What is the difference between a hard inquiry and a soft inquiry?" and "How can I remove a hard inquiry from my credit report?" With insights into credit reporting practices and actionable tips, you'll be better equipped to navigate the complexities of credit management.

Read also:Terry Kath The Underrated Guitar Legend Of Chicago

Table of Contents

- What Is a Hard Inquiry and Why Does It Matter?

- How Long Does a Hard Inquiry Stay on Your Credit Report?

- What Impact Does a Hard Inquiry Have on Your Credit Score?

- Hard Inquiry vs. Soft Inquiry: What's the Difference?

- Can You Remove a Hard Inquiry from Your Credit Report?

- Strategies to Minimize the Impact of Hard Inquiries

- Frequently Asked Questions About Hard Inquiries

- Conclusion: Managing Hard Inquiries for Better Credit Health

What Is a Hard Inquiry and Why Does It Matter?

A hard inquiry, also known as a "hard pull," is a credit check initiated by a lender when you apply for credit. This process involves the lender requesting your credit report from one or more credit bureaus to assess your creditworthiness. Hard inquiries are typically associated with significant financial transactions, such as applying for a mortgage, auto loan, personal loan, or credit card. Unlike soft inquiries, which are initiated for background checks or pre-approved offers, hard inquiries are recorded on your credit report and can influence your credit score.

Why does this matter? Hard inquiries provide lenders with a snapshot of your financial behavior, helping them decide whether to approve your application. However, these inquiries are not without consequences. Each hard inquiry can slightly lower your credit score, and multiple inquiries within a short timeframe may raise red flags for lenders. For example, applying for several credit cards in quick succession could signal financial distress, potentially affecting your ability to secure favorable loan terms.

Understanding hard inquiries is the first step toward managing their impact. While they are a necessary part of the credit application process, it's important to be strategic about when and how often you allow lenders to perform hard pulls. By doing so, you can minimize their effect on your credit score and maintain a strong financial profile.

How Long Does a Hard Inquiry Stay on Your Credit Report?

One of the most common questions borrowers ask is, "How long does a hard inquiry stay on your credit report?" The answer is straightforward: hard inquiries remain visible on your credit report for two years. However, their impact on your credit score diminishes over time. Most credit scoring models, such as FICO and VantageScore, only consider hard inquiries from the past 12 months when calculating your score. This means that while the inquiry stays on your report for two years, its influence on your creditworthiness typically fades within the first year.

Why does this timeframe matter? Lenders use your credit report to assess your financial behavior, and hard inquiries provide insight into how often you're applying for credit. Frequent hard inquiries can suggest financial instability, which may deter lenders from approving your application. For instance, if you apply for multiple credit cards or loans within a short period, lenders might view you as a higher-risk borrower, even if the inquiries occurred more than a year ago.

To mitigate the impact of hard inquiries, it's essential to space out your credit applications. For example, if you're shopping for a mortgage or auto loan, try to complete all applications within a 14-45 day window, depending on the credit scoring model. During this period, multiple inquiries for the same type of loan are often treated as a single inquiry, reducing their cumulative effect on your credit score.

Read also:Who Is Pauline Moran Young Discovering Her Life And Achievements

What Happens After Two Years?

After two years, hard inquiries are automatically removed from your credit report. This removal is part of the credit reporting process, ensuring that outdated information doesn't unfairly influence your credit score. While the inquiry itself is no longer visible, its initial impact on your score would have already diminished within the first year.

Can Hard Inquiries Be Removed Before Two Years?

Many borrowers wonder, "Can hard inquiries be removed from my credit report before the two-year mark?" The short answer is yes, but only under specific circumstances. If a hard inquiry was made without your consent or due to an error, you can dispute it with the credit bureau. Providing documentation to support your claim can expedite the removal process, helping you maintain a cleaner credit report.

What Impact Does a Hard Inquiry Have on Your Credit Score?

Understanding the impact of a hard inquiry on your credit score is crucial for maintaining financial health. While a single hard inquiry may only lower your score by a few points, multiple inquiries can compound the effect, potentially leading to a more significant drop. Credit scoring models like FICO and VantageScore consider hard inquiries as a factor in determining your creditworthiness. However, the exact impact varies based on your overall credit profile.

For individuals with a limited credit history or a low credit score, the impact of a hard inquiry can be more pronounced. Lenders view these borrowers as higher-risk, and a hard inquiry may further exacerbate their financial challenges. On the other hand, borrowers with a long and stable credit history may experience minimal effects from a single inquiry. For example, someone with a high credit score and a diverse credit mix may see only a negligible drop, if any, after a hard inquiry.

To minimize the impact, it's essential to monitor your credit report regularly and avoid unnecessary credit applications. Additionally, timing your applications strategically can help. For instance, if you're planning to apply for a mortgage or auto loan, try to limit other credit applications in the months leading up to your application. This approach ensures that your credit score remains as strong as possible during critical financial transactions.

How Many Points Does a Hard Inquiry Affect Your Score?

On average, a hard inquiry can lower your credit score by 5-10 points. However, this impact is temporary and diminishes over time. By maintaining responsible credit habits, such as making timely payments and keeping credit utilization low, you can offset the effects of a hard inquiry and rebuild your score quickly.

Hard Inquiry vs. Soft Inquiry: What's the Difference?

One of the most common areas of confusion for borrowers is the difference between hard and soft inquiries. While both involve checking your credit report, their purposes and impacts are vastly different. A hard inquiry occurs when a lender reviews your credit report as part of a credit application process. This type of inquiry is recorded on your credit report and can affect your credit score. Examples include applying for a mortgage, auto loan, or credit card.

In contrast, a soft inquiry is a credit check that does not impact your credit score. These inquiries are typically initiated for background checks, pre-approved offers, or when you check your own credit report. Employers may also perform soft inquiries during the hiring process to assess your financial responsibility. Since soft inquiries are not associated with credit applications, they are not visible to lenders and do not influence your creditworthiness.

Understanding the distinction between hard and soft inquiries can help you manage your credit more effectively. For example, checking your credit report regularly using a soft inquiry allows you to monitor your financial health without risking your credit score. Conversely, being mindful of hard inquiries ensures that you apply for credit strategically, minimizing their impact on your overall financial profile.

Why Are Soft Inquiries Harmless?

Soft inquiries are harmless because they do not signal financial distress to lenders. Since they are not tied to credit applications, they do not indicate an increased need for credit. This makes them a safe and practical way to stay informed about your credit status without jeopardizing your score.

Can You Remove a Hard Inquiry from Your Credit Report?

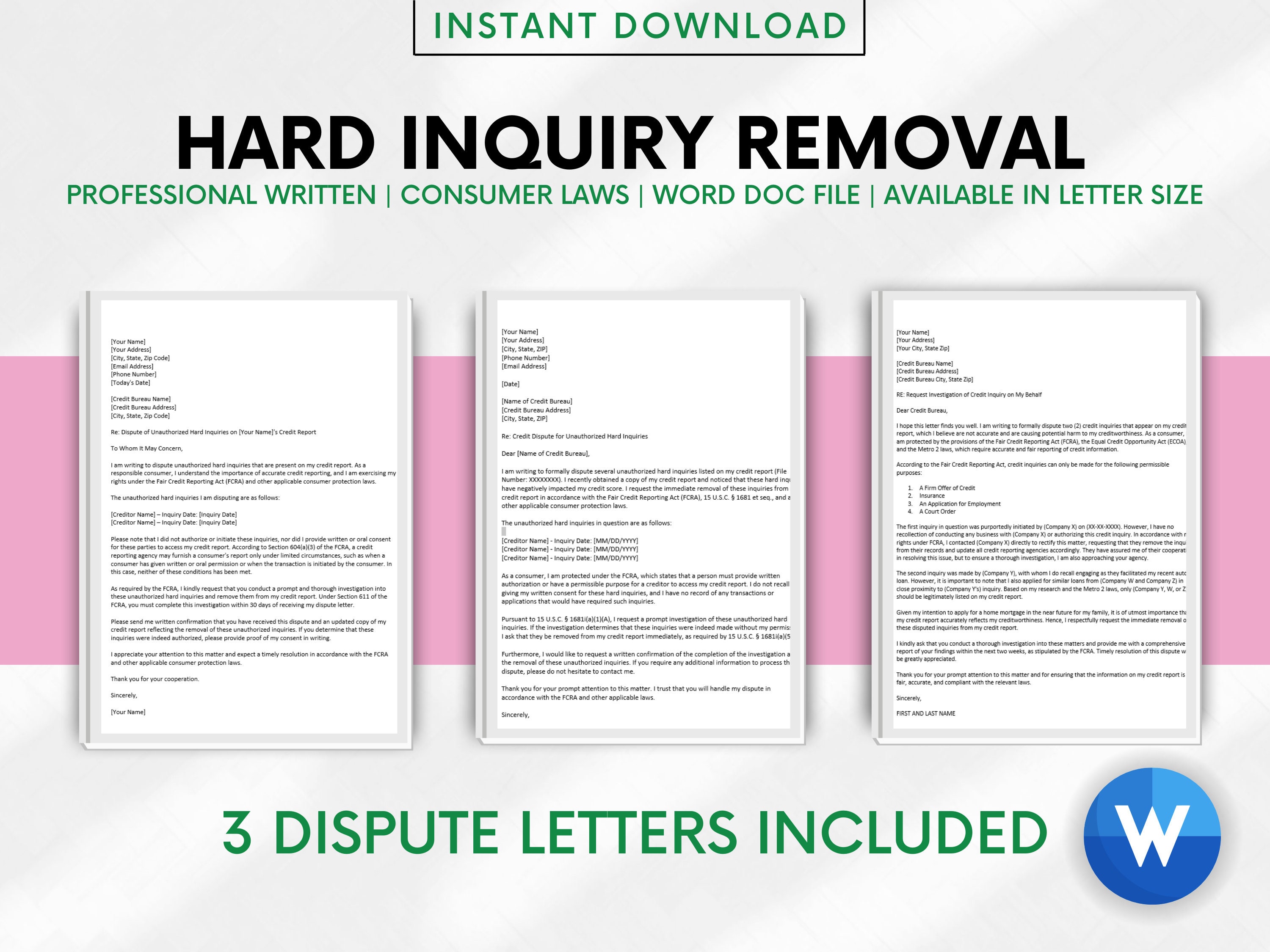

If you're concerned about hard inquiries on your credit report, you may be wondering, "Can you remove a hard inquiry from your credit report?" The answer is yes, but only under certain conditions. If a hard inquiry was made without your permission or due to an error, you have the right to dispute it with the credit bureau. This process involves submitting a formal dispute letter and providing supporting documentation to validate your claim.

To initiate a dispute, start by obtaining a copy of your credit report from all three major credit bureaus: Equifax, Experian, and TransUnion. Review each report carefully to identify any unauthorized or incorrect hard inquiries. Once identified, draft a dispute letter outlining the issue and include copies of relevant documents, such as proof of identity or correspondence with the lender. Submit your dispute to the appropriate credit bureau, and they will investigate the matter within 30 days.

If the investigation confirms that the hard inquiry was unauthorized or inaccurate, it will be removed from your credit report. However, if the inquiry was legitimate, it will remain on your report for the full two-year period. To avoid unnecessary hard inquiries in the future, always verify the purpose of a credit check before granting permission. This proactive approach ensures that your credit report remains accurate and reflects your true financial behavior.

What Documentation Is Needed to Dispute a Hard Inquiry?

When disputing a hard inquiry, you'll need to provide documentation to support your claim. This may include a copy of your credit report with the disputed inquiry highlighted, a letter explaining the issue, and any additional evidence, such as correspondence with the lender or proof of identity. Providing thorough documentation increases the likelihood of a successful dispute resolution.

Strategies to Minimize the Impact of Hard Inquiries

While hard inquiries are an inevitable part of the credit application process, there are several strategies you can use to minimize their impact on your credit score. One effective approach is to space out your credit applications. Applying for multiple credit accounts within a short period can signal financial instability to lenders, potentially lowering your credit score. By spacing out your applications, you allow time for the impact of each inquiry to diminish before applying for new credit.

Another strategy is to take advantage of rate shopping windows. When shopping for a mortgage, auto loan, or student loan, multiple inquiries for the same type of loan are often treated as a single inquiry if they occur within a specific timeframe. For FICO scores, this window is typically 14-45 days, while VantageScore allows a 14-day window. By completing all your applications within this period, you can minimize the cumulative effect of hard inquiries on your credit score.

Additionally, maintaining a strong credit profile can help offset the impact of hard inquiries. This includes making timely payments, keeping credit utilization low, and maintaining a diverse mix of credit accounts. By focusing on these positive credit behaviors, you can ensure that the temporary dip caused by a hard inquiry has minimal long-term consequences.

How Can You Monitor Your Credit Effectively?

Monitoring your credit regularly is an essential part of managing hard inquiries. Use free credit monitoring services or request your annual credit report from each bureau to stay informed about your financial health. By staying vigilant, you can quickly identify and address any unauthorized inquiries or errors on your report.

Frequently Asked Questions About Hard Inquiries

How Long Does a Hard Inquiry Stay on Your Credit Report?

Hard inquiries remain on your credit report for two years but typically only affect your credit score for the first 12 months. After this period, their impact diminishes significantly, and they are eventually removed from your report.

Does Checking Your Own Credit Count as a Hard Inquiry?

No, checking your own credit report is considered a soft inquiry and does not affect your credit score. It's a safe way to monitor your financial health without risking your creditworthiness.

Can Multiple Hard Inquiries Be Grouped Together?

Yes, multiple hard inquiries for the same type of loan